For waste operators, municipalities, and technology vendors, understanding where this market stands today — and where it's heading — matters. Investment decisions, vendor selection, and operational planning all benefit from a clear view of market size, growth trajectories, and the trends reshaping how waste fleets and municipal programs run.

This article covers the latest market data, the four most consequential trends, the forces driving growth, and the signals pointing to what comes next.

Key Takeaways

- The global waste management software market is valued at $11.97 billion in 2026, projected to reach $15.74 billion by 2030

- AI-powered route optimization, cloud migration, and IoT-connected infrastructure are the dominant forces reshaping fleet operations

- North America holds the largest regional market share, driven by compliance requirements and municipal digitization investment

- Tightening ESG and environmental regulations are accelerating enterprise adoption of digital compliance tools

- Vendor consolidation is accelerating as the market shifts from back-office software to core operational infrastructure

Waste Management Software Market: Size and Growth Outlook

Current Market Valuation

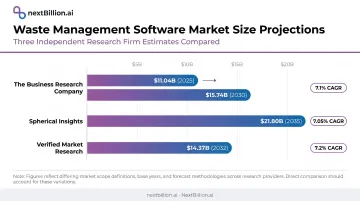

According to The Business Research Company's January 2026 report, the global waste management software market reached $11.04 billion in 2025, growing to an estimated $11.97 billion in 2026 at an 8.4% CAGR. Projections point to $15.74 billion by 2030 at a 7.1% CAGR.

Other forecasting firms use different market scope definitions and arrive at different baselines — Spherical Insights projects the market reaching $21.80 billion by 2035 at a 7.05% CAGR, while Verified Market Research estimates $14.37 billion by 2032 at 7.2%. The spread reflects scope differences in what each firm classifies as "waste management software" — not disagreement on direction. Every forecast points the same way: steady, sustained growth through the 2030s.

North America's Market Position

North America holds the largest regional share, with estimates ranging from approximately 36% to 43% depending on the source. The U.S. accounts for more than 75% of North America's share, according to Spherical Insights.

Regulatory maturity, infrastructure investment, and urban growth pressures all reinforce that position:

- Established compliance frameworks, including EPA's Resource Conservation and Recovery Act (RCRA)

- Mature municipal recycling infrastructure requiring digital coordination

- Heavy investment in smart city programs that incorporate waste operations

- Growing urban waste volumes demanding more efficient fleet management

Software Segments and End Users

The market spans several software categories, with municipal applications accounting for approximately 40.5% of market share (Spherical Insights). Key software types include route management, waste hauling, waste tracking, recycling, scale management, and maintenance software.

Primary end-user segments include:

- Municipalities and public works departments

- Private waste haulers and collection companies

- Healthcare and hospital waste programs

- Manufacturing facilities with industrial waste streams

- Retail and commercial property operators

Cloud-based deployment has become the dominant model, with multiple sources consistently reporting 61–63% of deployments now cloud-based. The shift comes down to economics: SaaS eliminates per-seat licensing fees and on-premise server costs, putting capable tools within reach of small and mid-size haulers who couldn't absorb the upfront expense of traditional installed systems.

Key Trends Reshaping the Waste Management Software Market

Trend 1: AI-Powered Route Optimization Is Becoming Standard

Static, manually planned routes are increasingly uncompetitive. AI-driven optimization now adjusts collection routes dynamically based on real-time variables — traffic conditions, fill levels, vehicle availability, driver hours, and service time windows — cutting fuel consumption, missed pickups, and overtime costs in one pass.

The results are measurable. The City of Franklin, Tennessee implemented RouteSmart route optimization and reported $1,083,812 in annual savings, a 37% reduction in operating expenses, and a shift from five-day to four-day residential collection. Academic research on municipal waste routing has found reductions in daily mileage of 25.44%, with data-driven optimization cutting vehicle kilometers traveled by up to 25% and diesel consumption by 10%.

What makes waste routing genuinely complex — and why generic mapping solutions fall short — is constraint density. Waste fleets must account for:

- Vehicle weight limits and turn restrictions for large trucks

- Time windows in residential and school zones

- Hazardous material classifications and landfill operating hours

- Multi-compartment vehicles handling source-separated recyclables

Platforms like NextBillion.ai address this complexity directly, offering 50+ hard and soft routing constraints through an API that waste software vendors can integrate into their own dispatch and scheduling platforms.

In a documented case study with SIR, a waste management provider operating in Mexico City, NextBillion.ai's Route Optimization API, Clustering API, and Geofencing capabilities delivered reduced fuel consumption, optimized vehicle-driver pairing, and customized routes that accommodated heavy truck restrictions across the fleet.

Trend 2: Cloud-Based Platforms Are Replacing Legacy Systems

The migration from on-premise software to cloud-based SaaS isn't a future trend — it's already the majority position. With ~62–63% of the market now cloud-deployed, the shift reflects practical realities:

- Lower upfront costs with no hardware investment

- Automatic updates without IT overhead

- Mobile access for drivers and field staff

- Scalable capacity without infrastructure changes

Denver's deployment of Rubicon smart city software across 150+ waste and recycling vehicles illustrates what cloud adoption looks like operationally — drivers moved from paper maps to a cloud-based system enabling real-time service tracking across the city's entire collection fleet.

Cloud adoption also enables end-to-end operational visibility that on-premise systems couldn't provide economically: live route tracking, customer billing, contract management, and regulatory reporting accessible from a single platform on any device.

Trend 3: IoT Integration and Smart Bin Technology Enable Data-Driven Collection

IoT sensors embedded in waste bins — fill-level sensors, RFID tags, weight sensors — are shifting collection from fixed-schedule runs to demand-based dispatch. When a bin reaches a defined fill threshold, it triggers a collection event rather than holding for a fixed calendar pickup.

According to Mordor Intelligence, the smart waste management market — which encompasses IoT-enabled collection infrastructure — is valued at $3.54 billion in 2025 and projected to reach $7.15 billion by 2030. Software platforms represent 41% of that market and are expected to grow at a 20.11% CAGR through 2030.

IoT holds a 35–40% share of waste management software as of 2026 (Verified Market Research), reflecting strong adoption across the stack. RFID and Real-Time Locating Systems (RTLS) are gaining particular traction in healthcare, manufacturing, and hazardous waste contexts, where chain-of-custody documentation is a compliance requirement, not just an operational preference.

Trend 4: ESG Reporting and Regulatory Compliance Are Driving Enterprise Adoption

That same data infrastructure is increasingly what regulators expect to see. Compliance has shifted from a software checkbox to a primary purchase driver — and two regulatory developments in 2026 make the pressure concrete:

- The EPA published a proposal on March 5, 2026 to phase out paper manifests and transition to a 100% electronic e-Manifest system for hazardous waste shipments

- The UK's digital waste tracking service enters public beta on April 28, 2026, with mandatory use starting October 2026 in England, Northern Ireland, and Wales

Beyond regulatory mandates, corporate ESG commitments are pushing enterprises to adopt software with built-in emissions reporting, audit-ready documentation, and carbon accounting integrations. Vendors offering compliance dashboards as core functionality — rather than an add-on module — win more enterprise deals.

What's Driving These Trends

No single factor explains the market's trajectory — several structural pressures are converging at once.

UNEP's 2024 Global Waste Management Outlook projects municipal solid waste rising from 2.1 billion tonnes in 2023 to 3.8 billion tonnes by 2050, with annual management costs potentially reaching $640.3 billion without urgent action. That scale of growth makes manual and legacy operations increasingly unworkable.

Five forces are accelerating the shift toward software:

- Volume pressure: More waste means more routes, more pickups, and more data — all of which manual systems handle poorly at scale.

- Technology accessibility: AI, IoT, and cloud infrastructure that once required large IT budgets are now available as API-driven services with per-vehicle or per-order pricing, bringing sophisticated routing and analytics within reach of mid-size haulers.

- Regulatory requirements: Stricter disposal rules, landfill diversion targets, EPR laws, and net-zero commitments require organizations to document measurable environmental outcomes — something spreadsheets and legacy systems can't deliver.

- Operational cost pressure: Rising fuel costs, labor shortages, and tighter municipal budgets make efficiency software financially urgent. Route optimization alone can materially reduce drive time, fuel consumption, and overtime.

- Smart city funding: As municipalities modernize infrastructure, digital waste operations are increasingly tied to performance benchmarks and funding eligibility.

Each driver reinforces the others. Regulatory pressure accelerates technology adoption; cost pressure builds the ROI case; rising waste volumes make the status quo untenable.

How These Trends Are Impacting the Waste Management Industry

Operational Impact

Route optimization and IoT-based dynamic scheduling are fundamentally changing how collection workflows are planned. Manual dispatch and paper-based processes are becoming operationally uncompetitive against teams using real-time routing and live fleet visibility.

The Franklin, Tennessee case study remains one of the most concrete public data points: $1.08 million in annual savings, a residential collection schedule compressed from five days to four, and a street sweeping cycle shortened from seven weeks to three — all from route optimization alone.

Routing infrastructure built for waste collection — handling vehicle weight limits, hazardous material routing, multi-compartment trucks, and dynamic resequencing mid-shift — is what converts those operational gains into real per-route cost reductions. NextBillion.ai's constraint-aware optimization API, for instance, supports all four of these requirements out of the box for waste fleet operators.

Business Impact

Waste companies and municipalities are moving away from point solutions toward integrated platforms spanning billing, compliance, customer management, and fleet operations.

Vendor consolidation reflects this shift:

- August 2024: Routeware acquired Wastech, which held Rubicon Smart City and Rubicon Pro, serving 100+ municipal heavy-duty fleets

- May 2025: AMCS acquired Selected Interventions and Mandalay Technologies — Selected Interventions' Echo framework supports residential waste services for 19 million residents globally

M&A activity of this pace signals a market moving toward fewer, more comprehensive platforms rather than a fragmented ecosystem of specialized tools.

Workforce Impact

Digital tools are reshaping the skills expected across waste operations. The role-level changes are tangible:

- Drivers and dispatchers work from mobile apps and live dashboards, not paper manifests

- Operations managers interpret route analytics in real time, not end-of-day reports

- Supervisors are accountable for software adoption outcomes, not just crew performance

The practical implication for organizations undergoing software transitions is that technology adoption requires deliberate change management — training programs, workflow redesign, and supervisor-level buy-in matter as much as the software selection itself.

Future Signals for Waste Management Software

Four converging forces — technology, regulation, electrification, and consolidation — are shaping where waste management software heads next.

Predictive scheduling shifts collection from reactive to anticipatory. Academic research published in 2025 explored machine learning for forecasting door-to-door municipal waste collection. The practical destination: routing systems that predict fill levels before bins are even scanned.

EV fleet integration has moved past the pilot stage. A 2024 study proposed routing formulations specifically for electric refuse trucks with range and charging constraints. Platforms like NextBillion.ai already support:

- Range-aware routing that accounts for battery state

- Automatic charging stop insertion mid-route

- EV-specific capacity and payload planning

These capabilities are becoming baseline requirements as municipalities electrify collection fleets.

Data interoperability is now a procurement differentiator. The UK's mandatory digital waste tracking — which requires API-based reporting — signals a broader direction: municipalities will increasingly demand that software vendors share data with city-wide digital infrastructure. Vendors with open API architectures will win those contracts.

Vendor consolidation reflects a structural shift toward end-to-end platforms. The M&A activity of 2024–2025 is deliberate, not cyclical. Larger vendors will continue acquiring point solutions in billing, routing, and IoT analytics, and pricing models will keep moving toward per-vehicle and outcome-based structures.

Frequently Asked Questions

What is waste management software used for?

Waste management software helps haulers, municipalities, and enterprises plan collection routes, manage fleet dispatch, track assets and compliance, handle customer billing and contracts, and report on recycling and environmental outcomes. Most platforms cover everything from daily scheduling to multi-year contract management in a single system.

How large is the waste management software market?

The market is valued at approximately $11.97 billion in 2026 and projected to reach $15.74 billion by 2030, based on The Business Research Company's January 2026 report. Growth is sustained by cloud adoption, regulatory compliance demands, and increasing urban waste volumes.

What features should you look for in waste management software?

Key capabilities to evaluate include route optimization, real-time fleet tracking, compliance and regulatory reporting tools, billing and customer management, and IoT or sensor integrations for dynamic scheduling. Multi-constraint routing support matters especially for mixed-fleet or hazardous waste operations.

What is driving growth in the waste management software market?

Primary drivers include rising urban waste volumes, stricter environmental regulations (EPA e-Manifest mandates, UK digital tracking requirements), and smart city investment. Operational cost pressure from fuel and labor — combined with more affordable AI and cloud tools — is pushing more operators to automate.

What is the difference between municipal and enterprise waste management software?

Municipal solutions focus on public service scheduling, citizen-facing features, regulatory compliance, and integration with city digital infrastructure. Enterprise solutions for private haulers prioritize billing, fleet profitability, contract management, and customer retention. The two segments share some overlap in routing and tracking, but their core operational goals diverge sharply.

How does AI improve waste management operations?

AI enables dynamic route optimization, predictive maintenance scheduling, contamination detection at point of collection, and demand-based scheduling triggered by IoT fill-level data. The result is lower fuel costs, fewer missed pickups, and reduced overtime compared to static, manually planned approaches.