Introduction

Running a non-emergency medical transportation business under Medicaid isn't just about having vehicles and drivers. You're operating under two simultaneous compliance frameworks: federal requirements established by Section 209 of the Consolidated Appropriations Act, and state-specific insurance mandates that vary considerably across jurisdictions.

Miss either one, and you're looking at suspended billing privileges, denied claims, or removal from provider networks entirely.

The stakes are real. An OIG audit found New York claimed $196 million — over 72% of the audited amount — in federal reimbursement for NEMT payments to NYC providers that did not meet or may not have met Medicaid requirements. A separate OIG review found Massachusetts made at least $14 million in improper Medicaid NEMT payments.

This guide is written for NEMT business owners and fleet operators — whether you're pursuing initial Medicaid enrollment or protecting existing provider status.

Key Takeaways

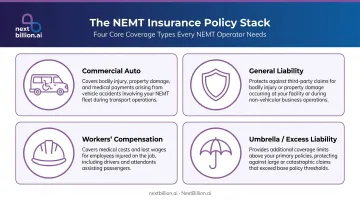

- NEMT providers need multiple distinct policies: commercial auto, general liability, workers' compensation, and often umbrella coverage

- Section 209 of the Consolidated Appropriations Act (2021) sets federal baseline requirements, but states like California and Illinois impose their own, often stricter, insurance minimums

- Insurance lapses trigger immediate billing suspension, claim denials, and potential MCO contract termination

- GPS-based trip documentation produces the audit-ready records Medicaid billing reviews and insurance claims require

What Insurance Coverage Does a Medicaid NEMT Provider Actually Need?

There's no single "NEMT insurance" product you purchase and check off a list. Providers typically need several distinct policies working together.

The Core Policy Stack

| Policy Type | What It Covers |

|---|---|

| Commercial auto insurance | Vehicles while in service — collisions, damage, third-party liability |

| General liability insurance | Passenger incidents not tied to vehicle accidents (slips, falls at pickup) |

| Workers' compensation | Driver injuries as employees |

| Umbrella/excess liability | Additional coverage layer to reach state-mandated minimums cost-effectively |

Why personal auto insurance won't work: Personal policies explicitly exclude vehicles used for hire or medical transport. A provider operating under a personal policy faces both denied claims after any incident and potential Medicaid disqualification. The Insurance Information Institute recommends $1 million in business auto coverage, with $500,000 as a minimum — though these are industry guidance figures, not Medicaid mandates.

Vehicle Type Affects Coverage Requirements

Not all vehicles in a NEMT fleet carry the same insurance profile:

- Standard sedans and minivans — baseline commercial auto coverage applies; premiums are lower but must still reflect commercial-use classification

- Wheelchair-accessible vehicles (WAVs) — higher premiums due to specialized lift equipment, ramp mechanisms, and greater passenger vulnerability

- Stretcher vans — typically the most expensive to insure, given the medical nature of transports and equipment involved

ADA Compliance and Coverage Validity

Vehicles serving disabled Medicaid patients must meet ADA accessibility standards under Title III regulations. ADA non-compliance doesn't automatically void insurance coverage as a matter of law, but it creates significant liability exposure after any incident and can jeopardize Medicaid enrollment.

Treat ADA compliance and insurance compliance as parallel obligations. Falling short on either front carries real consequences — one affects your legal exposure, the other your program eligibility.

Subcontracted Drivers and TNC Models

Operations using subcontracted drivers or transportation network company (TNC) arrangements face coverage gaps that are harder to track and assign. CMS guidance applies provider and driver screening requirements to both NEMT providers and individual drivers — subcontractors are not exempt.

Before any subcontractor transports a patient, confirm:

- Their commercial auto policy meets your state's Medicaid minimums

- They carry adequate general liability coverage

- Their driver screening documentation matches your own program requirements

Gaps in a subcontractor's coverage can expose the primary provider. Verify compliance upfront — not after an incident.

Federal Baseline vs. State-Specific NEMT Insurance Requirements

The Federal Floor

42 CFR § 431.53 requires every state Medicaid plan to assure necessary transportation for beneficiaries to and from providers.

Section 209 of the Consolidated Appropriations Act (2021) added Section 1902(a)(87) to the Social Security Act, requiring state plans to include mechanisms ensuring NEMT providers meet minimum standards — covering driver license validity, exclusion from federal healthcare programs checks, and processes for disclosing driver violations.

The key federal reference document is CMS SMD 23-006, titled "Assurance of Transportation: A Medicaid Transportation Coverage Guide," issued September 28, 2023. It consolidates federal transportation policy and clarifies state flexibilities, including how states may pay for transportation as either an administrative expense or optional service. Read it before any state-level enrollment work.

This federal framework is a floor, not a ceiling. States regularly set higher requirements.

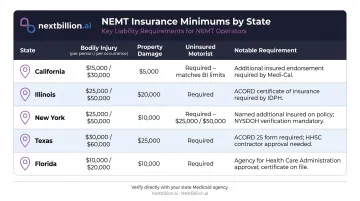

State-by-State Insurance Minimums

Requirements vary significantly. Always verify directly with your state Medicaid agency, as minimums change:

| State | Verified Insurance Requirement | Source |

|---|---|---|

| California | Commercial liability: $100,000 per claim / $300,000 annual aggregate; workers' compensation where applicable | CA DHCS provider application |

| Illinois | Vehicle liability: $100,000 per person / $300,000 per accident / $50,000 property damage; HFS must be named additional insured; 30-day cancellation notice required | IL HFS New Provider Checklist |

| New York | Providers credential through the centralized MAS system; must upload ACORD insurance forms including general liability, workers' comp, and NYS disability insurance | MAS Transportation Provider Network Manual |

| Texas | Current driver license, valid registration, and car insurance required for individual transportation participants | TX HHSC / TMHP |

| Florida | Providers must meet applicable licensure and regulatory requirements per AHCA policy | FL AHCA NET coverage policy |

Important: Dollar minimums for Florida and Texas were not confirmed in official state Medicaid sources during research. Contact those state agencies directly for current requirements.

Broker Requirements Add Another Layer

State Medicaid minimums aren't the only standard you'll face. NEMT brokers — Modivcare, MTM, SafeRide Health, and others — typically impose their own insurance thresholds and endorsement requirements as a condition of trip assignment. These requirements appear in your broker contract, not in state plan documents.

Review broker contracts line by line alongside state requirements. You can be fully compliant with state Medicaid and still fail a broker credentialing review due to a missing endorsement or insufficient coverage limit.

Multi-state operators face the heaviest administrative load. Each state's requirements are independent, and the variables compound quickly:

- Renewal cycles differ across jurisdictions

- Minimum thresholds can change year to year

- Broker contracts may impose separate requirements per state

- Documentation sets must be maintained independently for each market

How to Achieve and Maintain Insurance Compliance

Getting Compliant Before Medicaid Enrollment

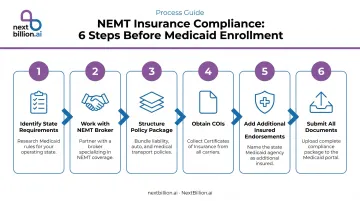

Follow these steps before submitting your provider application:

- Identify state requirements — Pull your state Medicaid agency's provider enrollment materials to confirm current insurance minimums, and request any additional requirements from broker networks you plan to join.

- Work with a commercial broker familiar with NEMT — A general commercial insurance broker may not know the difference between standard commercial auto and medical transport coverage. Find one with NEMT or medical transportation experience.

- Structure the right policy package — At minimum, you need commercial auto, general liability, and workers' comp. Add umbrella coverage if needed to hit state minimums cost-effectively.

- Obtain Certificates of Insurance (COIs) — Get ACORD-format COIs listing policy numbers, effective and expiration dates, insurer name, and coverage limits.

- Add required additional insured endorsements — Illinois, for example, requires HFS to be named as additional insured. Many MCOs require the same. Missing this endorsement is one of the most common causes of application delays.

- Submit all COIs with your enrollment application — include every required insurance document in the initial package.

Ongoing Compliance Maintenance

Enrollment gets you in the door. Staying compliant after enrollment is where most providers slip up:

- Set renewal reminders at least 60 days out — Don't wait for expiration notices

- Distribute updated COIs after every renewal — Send to all active brokers and MCO partners immediately

- Notify your state Medicaid agency immediately if coverage lapses, is canceled, or drops below required minimums — most programs require prompt disclosure

- Update policies before new vehicles enter service — Adding a WAV, retiring a sedan, or swapping vehicle types triggers immediate documentation obligations

- Resubmit updated COIs to Medicaid and all broker networks before the new vehicle transports a single patient

What Happens When NEMT Insurance Non-Compliance Occurs

Immediate Operational Consequences

The response to an insurance lapse is typically fast:

- Medicaid programs can immediately suspend billing privileges

- Pending claims may be denied — including claims for trips already completed

- Brokers can revoke trip assignment authorization — trips in progress may go unreimbursed

Longer-Term Business Consequences

Repeated or serious insurance compliance failures create consequences that outlast any single coverage gap:

- Permanent disenrollment from the state Medicaid program

- Exclusion from federal healthcare programs through the OIG exclusions process

- MCO contract termination across multiple broker relationships

The OIG's improper payment findings in New York and Massachusetts (totaling over $210 million combined) illustrate how aggressively federal and state agencies pursue NEMT compliance failures. Those audits weren't insurance-specific, but they confirm that NEMT providers operate under continuous program integrity scrutiny — one lapse can trigger a broader review of your entire billing history.

Liability Beyond Medicaid

Operating an NEMT vehicle without compliant commercial insurance creates direct personal and business financial exposure. If an accident occurs during a coverage gap, there's no policy to cover the claim — the liability falls on the business directly.

Beyond accident risk, billing Medicaid for trips completed during a coverage gap draws program integrity scrutiny. Auditors don't distinguish between intentional fraud and administrative oversight. Either way, providers face recoupment demands and potential exclusion proceedings.

How Route Tracking Technology Supports NEMT Insurance Compliance

The Documentation Problem

Both NEMT insurers and Medicaid auditors require verifiable proof of trip completion — pickup time, route taken, actual mileage, and drop-off confirmation. Paper logs and manual entries are difficult to defend during an audit and easy to challenge in an insurance dispute. A timestamped digital record of every trip changes that dynamic entirely.

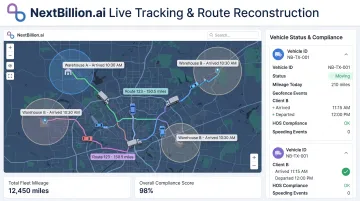

What GPS Tracking Captures

NextBillion.ai's Live Tracking API provides real-time vehicle tracking with up to 1-meter accuracy, capturing the data points that compliance reviews actually require:

- Geofence-based arrival and departure timestamps at pickup and drop-off locations

- Actual route path versus planned route — route deviation alerts flag unauthorized departures from assigned routes

- Automated mileage reporting for billing verification and reimbursement calculations

- Proof-of-service documentation that supports Medicaid billing compliance and state/broker contract requirements

The Route Reconstruction API takes raw GPS breadcrumb sequences and transforms them into complete, road-snapped, audit-defensible trip records — every road taken, every waypoint, every distance, mapped to the actual road network. It's built for regulated industries that need verifiable trip history, including NEMT proof-of-service.

Real-World NEMT Application

NextBillion.ai works with Ride Care, a NEMT operator serving the Oklahoma Department of Mental Health and Substance Abuse Services. Before implementing NextBillion.ai's routing and dispatch tools integrated with Samsara, Ride Care's team was manually assembling trips using sticky notes and working half the night to build workable schedules.

After integration, the same planning process takes under two hours. Optimized routes dispatch directly into drivers' Samsara apps, eliminating the manual data entry errors that most often compromise trip records during audits.

The platform also supports HIPAA-compliant workflows, cost-per-trip tracking, and billing and compliance reporting — including the ability to regenerate accurate data for completed trips specifically for billing and compliance reviews.

Fraud Prevention Through GPS Verification

GPS-verified mileage prevents overbilling disputes with both Medicaid and insurers. Route anomaly detection identifies when drivers deviate from planned routes, which matters for two reasons: unauthorized deviations can void insurance coverage under some policy terms, and mileage discrepancies between planned and actual routes are a common trigger for Medicaid billing audits.

That audit risk is compounded when compliance data lives across multiple telematics platforms. NextBillion.ai's integrations with Samsara, Geotab, and Motive consolidate trip records into a single system — so when an auditor requests documentation, the data is already in one place rather than scattered across disconnected sources.

Frequently Asked Questions

How much does NEMT insurance cost per month?

NEMT insurance premiums vary based on fleet size, vehicle types, state of operation, driver history, and required coverage limits. WAVs and stretcher vans typically cost more to insure than standard sedans due to specialized equipment and greater liability exposure. Industry guidance suggests business auto limits of $500,000 to $1 million as a starting point — contact an NEMT-specialized broker for quotes based on your specific fleet profile and state requirements.

How do I become a Medicaid-approved NEMT provider?

Research your state Medicaid agency's transportation provider requirements, then obtain the required insurance coverage with correct limits and endorsements. Complete the Medicaid provider enrollment application with all supporting documentation, including COIs. If your state contracts through a broker like Modivcare or MTM, complete their separate credentialing process as well.

Does Medicaid pay for NEMT?

Yes. Under 42 CFR § 431.53, states must assure transportation for Medicaid beneficiaries. Coverage is provided either as an administrative expense or optional service depending on the state. Reimbursement is contingent on the provider meeting all enrollment and insurance compliance requirements.

What types of insurance does an NEMT provider need?

Most NEMT providers need four core coverage types:

- Commercial auto insurance — covers vehicles actively in service

- General liability insurance — covers passenger incidents outside vehicle accidents

- Workers' compensation — required for employed drivers in most states

- Umbrella or excess liability — often needed to meet state minimum limits cost-effectively

What happens if an NEMT provider lets their insurance lapse?

A lapse can trigger immediate suspension of Medicaid billing privileges, claim denials for trips taken during the gap, and revocation of MCO trip assignments. Most state Medicaid programs require providers to notify the agency immediately of any coverage change. Reinstatement typically requires proof of restored coverage and may involve a compliance review before billing privileges are restored.