Introduction

Route optimization software has crossed a clear threshold. What was once a competitive advantage for large logistics operators is now a baseline requirement for any fleet-dependent business trying to remain solvent.

The numbers back this up. According to Future Market Insights, the global route optimization and planning software market sits at $7.6 billion in 2025 — and that figure is climbing fast. E-commerce parcel volumes hit 22.37 billion shipments in the US alone in 2024, according to the Pitney Bowes Parcel Shipping Index. Manual route planning simply cannot keep pace with that scale.

That gap is exactly what this report addresses. Logistics leaders, fleet managers, and software buyers will find a grounded view of where the market stands heading into 2026 — its size, growth trajectory, regional dynamics, and what the data means for purchasing decisions.

TLDR: Key Takeaways

- The global market is valued at $7.6B in 2025, projected to reach $22.5B by 2035 at an 11.5% CAGR

- North America leads in market share; Asia-Pacific is the fastest-growing region at ~15% CAGR

- Cloud-based (SaaS) solutions dominate, capturing an estimated 72.4% of 2025 revenue

- E-commerce growth and last-mile delivery complexity are the primary demand catalysts

- Per-vehicle and per-order pricing are displacing per-API-call billing across serious enterprise buyers

Route Optimization Software Market Size: Where It Stands in 2026

The 2025 Baseline and Forecast

Future Market Insights pegs the route optimization and planning software market at $7.6 billion in 2025, growing to $22.5 billion by 2035 at an 11.5% CAGR. A separate Grand View Research report places the 2030 market value at $21.46 billion, consistent with the broader trajectory.

For context, route optimization sits within a much larger logistics technology stack:

| Segment | 2030 Market Forecast | CAGR |

|---|---|---|

| Fleet Management | $70.26 billion | ~10% |

| Transportation Management Systems | $37 billion | ~9% |

| Route Optimization Software | $21.46 billion | 11.5% |

Route optimization is a focused sub-segment — and it's growing faster on a percentage basis than most observers expected five years ago.

Why 2026 Looks Like an Inflection Point

The 2020–2025 arc tells the story. The COVID-19-driven e-commerce surge forced millions of businesses to scale up delivery operations practically overnight. Many cobbled together manual processes or basic mapping tools to survive.

Those workarounds didn't hold. As delivery volumes normalized at permanently higher levels, investment in purpose-built optimization software accelerated sharply.

The ROI case is unusually clear-cut. Fuel accounts for 21.3% of average trucking operating costs ($0.481 of every $2.26 per mile driven, per ATRI's 2024 analysis). Shaving even 5–10% off total miles driven through better routing produces measurable savings at fleets of 10 vehicles or more. Across thousands of operators running that calculation, a $7.6 billion market starts to make obvious sense.

The Dynamic Routing Sub-Segment

The dynamic route optimization sub-market — real-time, continuously updated routing rather than batch-processed overnight plans — was valued at approximately $1.9 billion in 2024 and is projected to grow at a 13.1% CAGR through 2034. That faster clip reflects a clear enterprise preference shift: static, overnight planning tools are giving way to systems that adapt to live traffic and same-day order changes as they happen.

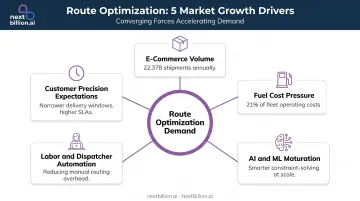

What's Driving Market Growth?

Five converging forces are expanding the route optimization software market — and they tend to amplify each other.

E-Commerce and Last-Mile Complexity

Amazon, DoorDash, Zepto, quick-commerce platforms — these operations have redefined what "normal" delivery looks like. More stops per route, tighter time windows, same-day or sub-hour expectations. A route that involves 40 stops with varied delivery windows is not a planning problem humans can solve optimally in any reasonable time. Algorithms can.

US parcel volume reached 22.37 billion shipments in 2024, up 3.4% year-over-year. Amazon Logistics alone handled 6.3 billion parcels in the US that year. The volume itself is only half the challenge — the density of constraints per stop is what makes manual planning unworkable.

Fuel Cost Pressure

With fuel representing over 21% of trucking operating costs, route efficiency has a direct P&L impact. PTV reports optimization-driven savings of 17% or more on route distance. Even conservative real-world results — 8–12% fewer miles driven — translate into material dollar savings for any fleet running more than 20 vehicles.

AI and Machine Learning Maturation

Early routing tools solved a simple shortest-path problem. Modern optimization engines handle real-time traffic, weather disruption, vehicle-specific constraints, driver skill matching, time window compliance, and dynamic re-routing mid-shift. That gap between 2015-era tools and current platforms is pushing enterprises to replace legacy systems rather than patch them.

Labor Pressures and Dispatcher Automation

Experienced dispatchers and route planners are difficult to hire and retain. Their knowledge also shouldn't live only in someone's head. Route optimization software encodes planning logic into repeatable, auditable processes — reducing dependence on any single person and enabling less experienced staff to manage more complex operations.

Key outcomes businesses report after automating dispatch:

- Faster route creation with fewer planning errors

- Consistent results regardless of who's on shift

- Easier onboarding for new planners and coordinators

Customer Expectations for Precision

Narrow delivery windows and real-time ETAs are now baseline expectations, not premium features. That pressure cascades directly to dispatchers and fleet managers. Businesses that can't promise and deliver accurate ETAs lose contracts to those that can.

Market Segmentation: Deployment, Application, and Region

By Deployment Type

| Deployment | 2025 Market Share | Key Driver |

|---|---|---|

| Cloud-based (SaaS) | ~72.4% | Lower upfront cost, faster deployment, easier integration |

| On-premise | ~27.6% | Data sovereignty, enterprise security requirements |

Cloud solutions dominate for straightforward reasons: no hardware, faster implementation, easier updates, and subscription pricing that converts capital expenditure into predictable operating expenditure. On-premise retains a meaningful role among large enterprises and government logistics operations with strict data control requirements. Some vendors, including NextBillion.ai, support both models — including deployment within a customer's own Kubernetes environment or private data center.

By Application and End-User Industry

Primary segments driving market revenue:

- Parcel and last-mile delivery — highest volume, most constraint-intensive use case

- Food delivery and quick commerce — highest frequency; stress-tests optimization systems more than any other vertical

- Field service management — pest control, HVAC, home healthcare, inspection services

- Freight and B2B distribution — multi-depot, load optimization, truck-specific routing

- Non-emergency medical transportation (NEMT) — time-sensitive, compliance-heavy scheduling

Route optimization has expanded well beyond traditional trucking. Healthcare logistics and field service now represent two of the fastest-growing segments — each with distinct scheduling constraints, but the same core requirement: algorithmic planning that scales with operational complexity.

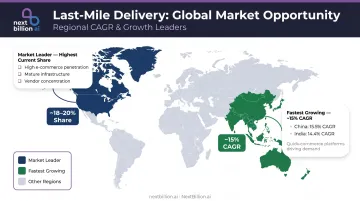

By Region

North America currently leads global market share, driven by:

- High e-commerce penetration and established logistics infrastructure

- Greater awareness of routing software ROI among fleet operators

- Concentration of major software vendors headquartered in the region

Asia-Pacific is the fastest-growing region. Grand View Research projects APAC growing at approximately 15% CAGR, with China forecast at 15.5% CAGR and India at 14.4% CAGR per Future Market Insights. The drivers are distinct from North America: rapid expansion of food delivery and quick-commerce platforms (Zepto, Meesho, Gojek, and their competitors), growing SME logistics operators seeking affordable cloud tools, and significant investment in logistics infrastructure across Southeast Asia.

Competitive Landscape: Key Players and Market Dynamics

The Vendor Mix

The market is moderately fragmented — no single vendor holds dominant share. The landscape breaks into three categories:

- Legacy enterprise vendors: Descartes, PTV Group (now Aptean/Paragon post-acquisition), Omnitracs, Trimble — established platforms with deep routing logic and broad enterprise relationships

- SaaS specialists: Route4Me (21,000+ customers), OptimoRoute, FarEye, Locus — mid-market focused, faster deployment

- API-first platforms: NextBillion.ai, Google Maps Platform, HERE Maps — developer-oriented, infrastructure-layer positioning

Where Legacy Vendors Leave Gaps

Legacy mapping providers charge per API call. Google's Compute Route Matrix API caps at 625 elements per request (or 100 elements for traffic-aware requests). The legacy Distance Matrix API caps at 25 origins × 25 destinations per request. At scale, these constraints force engineers to batch requests, increasing latency and cost unpredictably.

NextBillion.ai targets this gap directly. Its Distance Matrix API handles matrices up to 5,000 × 5,000 elements, accommodates 50+ routing constraints, and prices on a per-vehicle or per-order basis rather than per API call.

The results are measurable: the platform has documented over $11 million in cost savings across 150+ enterprise customers globally, with individual customers reporting API cost reductions of 30–82% after switching from Google Maps.

Customers like TruckIT, Hawx Pest Control, and Printo switched primarily for three reasons: matrix scale limitations at Google, unpredictable API billing at volume, and the absence of truck-specific routing constraints in generic mapping platforms.

Consolidation Signals

Aptean's acquisition of UK-based Paragon Software Systems (completed 2020) marked an early consolidation signal in the enterprise routing segment. In 2025, NextBillion.ai became part of Velocitor Solutions, combining AI-driven routing and mapping with Velocitor's established fleet telematics and real-time visibility platforms. Both brands continue operating independently while building toward a combined platform spanning routing, dispatch, and real-time fleet visibility.

For buyers, consolidation means fewer standalone point solutions and more integrated platforms — but also higher switching costs once embedded. Before committing, assess how deeply a vendor's routing data, APIs, and historical records can transfer if you need to migrate.

Emerging Trends Shaping the Market Through 2030

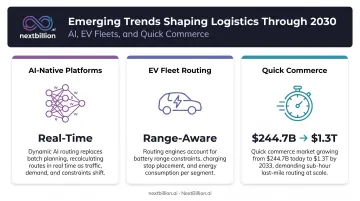

AI-Native Platforms Replacing Legacy Optimization Engines

The gap between batch-processed overnight route plans and real-time, continuously updated routing is widening. Enterprises running static planning tools are hitting a hard operational ceiling: missed time windows, no capacity to insert ad hoc orders mid-shift, zero response to live traffic disruption. Vendor evaluation cycles are compressing as a result — procurement teams that reviewed routing software every three to five years are now reassessing annually.

EV Fleet Routing

As logistics operators transition to electric vehicles, route optimization software must handle range constraints, charging stop planning, and battery management. For any fleet already running EV assets, this is a current procurement requirement — not a roadmap item. NextBillion.ai, for example, already supports:

- Smart charging stop integration within multi-stop route plans

- Battery capacity optimization across mixed fleets

- Vehicle-specific route customization by EV model

Quick Commerce and Hyperlocal Demand

The quick-commerce market was valued at $244.7 billion in 2025 and is projected to reach $1.3 trillion by 2033 at a 23.5% CAGR, per Grand View Research. Sub-30-minute delivery, NEMT scheduling, and real-time field dispatch are pushing the entire route optimization market toward higher-frequency, lower-latency algorithmic performance. Five years ago, this level of throughput at commercial scale wasn't viable. It is now.

What This Market Growth Means for Fleet and Logistics Buyers

A growing, competitive market benefits buyers — more options, faster feature development, and downward pricing pressure. But the same market growth also floods the category with underpowered tools that won't survive real-world operational complexity.

Three evaluation criteria separate serious platforms from noise:

1. Pricing Model Transparency

The per-API-call model creates unpredictable costs at scale. Buyers in 2026 should look for per-vehicle or per-order pricing. NextBillion.ai's model — which scales unit pricing down as monthly volume increases — gives finance teams the predictability that per-call billing cannot. Usage alerts at 50%, 75%, and 90% thresholds mean no billing surprises.

2. Constraint Depth

A routing tool that handles 10 constraints works fine for simple fleets. A tool that handles 50+ — vehicle dimensions, time windows, skills-based driver matching, hazmat compliance, multi-depot coordination, load sequencing — handles the real world. That gap is the difference between software that trims inefficiency and software that overhauled how you dispatch.

3. Integration Ecosystem

Route optimization software that connects natively with Samsara, Geotab, and Motive (as NextBillion.ai does) creates bidirectional data flow: telematics data feeds the optimizer, optimized routes push back to driver apps. That closed loop eliminates manual CSV exports and reduces dispatcher workload.

Standalone tools that require manual data transfer between systems create more friction than they remove.

How quickly a platform deploys is the fourth factor most buyers underweight. NextBillion.ai customers have gone from evaluation to production in as little as 10 days. Legacy enterprise vendors often quote multi-month implementation timelines — and every month without optimization is a month of avoidable fuel spend, dispatcher overload, and missed delivery windows.

Frequently Asked Questions

What is the current size of the route optimization software market?

The market is valued at approximately $7.6 billion in 2025, projected to reach $22.5 billion by 2035 at an 11.5% CAGR, per Future Market Insights.

Which region dominates the route optimization software market?

North America currently leads due to high e-commerce penetration, mature logistics infrastructure, and strong vendor concentration. Asia-Pacific is the fastest-growing region, forecast at approximately 15% CAGR, driven by quick-commerce expansion in India, China, and Southeast Asia.

What are the main growth drivers for route optimization software?

Three factors are driving growth:

- E-commerce and last-mile delivery volume continuing to climb

- Fuel cost pressure (fuel exceeds 21% of trucking operating costs)

- AI/ML advancement enabling real-time dynamic optimization that legacy tools can't match

What is the difference between cloud-based and on-premise route optimization software?

Cloud-based (SaaS) solutions offer lower upfront cost, faster deployment, and easier integration — they account for roughly 72% of 2025 market revenue. On-premise suits large enterprises with strict data sovereignty requirements, supporting deployment within Kubernetes environments or private data centers.

Which industries benefit most from route optimization software?

Last-mile and parcel delivery, food and quick-commerce platforms, field service operations (HVAC, pest control, home healthcare), freight distribution, and NEMT. High-frequency use cases like food delivery and on-demand logistics place the greatest demands on optimization systems.

How should businesses evaluate route optimization software vendors in 2026?

Prioritize these four criteria:

- Pricing transparency: per-vehicle or per-order models over per-API-call billing

- Constraint depth: 50+ constraints for complex multi-stop operations

- Integration capability: compatibility with existing telematics and fleet management systems

- Support quality: solution engineers available during implementation, not just post-sale