That approach fails. Latin America's informal road networks, cash-first payment culture, and city-by-city regulatory patchwork require software built for local realities — not adapted from other markets. This guide covers the market opportunity, the competitive landscape, the operational challenges that actually trip up operators, and the software capabilities that matter most for LATAM deployments.

Key Takeaways

- Latin America's ride-sharing market was estimated at $4.31B in 2024, growing at a 19.3% CAGR — with significant room for regional and niche operators

- Uber, DiDi, and Cabify dominate major metros but leave secondary cities and underserved segments largely uncontested

- LATAM-specific challenges — informal road networks, cash payments, fragmented city-level regulation — demand software purpose-built for these conditions

- Non-negotiable software capabilities include cash trip workflows, vehicle-type-specific routing, offline navigation, and custom map editing for informal settlements

- Stack decisions (build vs. white-label vs. API-layer) directly affect time-to-market and platform scalability

Why Latin America Is a High-Growth Market for Ride-Hailing

Market research estimates put the Latin America ride-sharing market at $4.31B in 2024, growing to $5.23B in 2025 and potentially reaching $17.85B by 2032 at a 19.3% compound annual growth rate. Three structural factors drive that trajectory: extreme urban density, chronically inadequate public transit, and fast-expanding smartphone penetration.

The Urban Density Advantage

According to World Bank data sourced from UN World Urbanization Prospects, approximately 81% of Latin America's population lives in urban areas — one of the highest urbanization rates of any developing region. That concentration of demand in cities is a core advantage for ride-hailing economics.

The transit situation in major metros amplifies this further. São Paulo's metro regularly operates beyond capacity. Bogotá's TransMilenio BRT has faced persistent overcrowding. Mexico City's informal transport networks leave significant coverage gaps.

This matters for operators: demand for ride-hailing in these cities isn't discretionary. Riders turn to apps because public transit genuinely falls short.

Where the Entry Opportunities Are

Not all LATAM markets are equal:

- Brazil and Mexico — largest by volume, dominated by established players, but still offer niche opportunities (corporate, women-only, mototaxi)

- Colombia and Chile — high-growth secondary markets with maturing regulatory frameworks

- Central America and secondary cities — lowest competitive density, highest opportunity for a localized operator to build market share before incumbents arrive

- Peru and Ecuador — underpenetrated relative to population size; Cabify has foothold, but secondary cities remain open

GSMA reports that mobile technologies generated $550B (8.2% of GDP) across Latin America in 2024, with smartphone infrastructure increasingly reaching peri-urban areas. For operators, that peri-urban reach translates directly into serviceable territory that wasn't viable two or three years ago.

Key Players Shaping the LATAM Ride-Hailing Landscape

The Big Three

| Player | Core Strength | Primary Markets |

|---|---|---|

| Uber | Regulatory benchmark, broadest coverage | Brazil, Mexico, Colombia, Chile, 15+ countries |

| DiDi | Aggressive pricing, large driver supply | Mexico, Brazil (via 99 acquisition) |

| Cabify | Premium and corporate positioning | Chile, Peru, Colombia, Spain-linked markets |

Uber functions as the region's de facto regulatory baseline — when a city drafts ride-hailing rules, Uber's operating model is typically the implicit reference. DiDi's 2018 acquisition of Brazilian app 99, valued above $1B according to Reuters, handed it instant scale in Brazil. Cabify raised $110M in March 2023 to deepen its foothold in premium and corporate travel across LATAM and Spain.

Where Incumbents Leave Room

Easy Taxi's consolidation into Cabify in 2017 eliminated one regional contender. The gap it left — particularly in Central America and secondary cities — remains largely unfilled. InDriver is making inroads with a price-negotiation model that resonates in cost-sensitive markets, but its presence in secondary Spanish-speaking cities is still developing.

Multi-homing is the norm in LATAM: riders and drivers routinely run multiple apps simultaneously. New entrants don't need to displace Uber to survive. Earning a slot in the user's rotation — through better driver economics, a niche service type, or stronger reliability in a specific geography — is enough.

Unique Challenges of Launching Ride-Hailing Software in LATAM

Fragmented and Inconsistent Mapping Data

UN-Habitat data shows that 24.4% of Latin America's urban population lived in informal settlements as of 2014 — a figure that represents tens of millions of potential riders in areas where official road data is incomplete, outdated, or simply wrong.

When a routing engine built on generic map data tries to navigate São Paulo's favelas or Mexico City's colonias populares, the results are predictable: missed pickups, incorrect ETAs, confused drivers, and cancellations that erode platform trust fast.

Software that supports custom road attribute editing addresses this directly. NextBillion.ai's Road Editor App, for example, lets operations teams add roads that don't exist on base maps, plot entry and exit points for settlements, set custom speed limits, and define vehicle-specific routing rules — all through a no-code interface that feeds live into the routing engine.

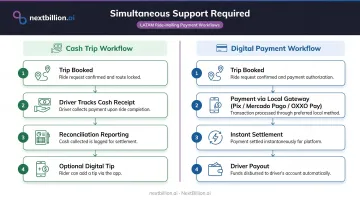

Cash-Dominant and Mixed Payment Ecosystems

Cash remains an active operational reality across LATAM, not a legacy holdover. Reuters documented that Uber only began accepting cash in Mexico City in 2018 after a Supreme Court decision, specifically because the market demanded it.

A year later, when Mexico City tried to ban cash payments, both Uber and DiDi pushed back — DiDi noted the policy would directly harm unbanked riders.

Brazil has moved further toward digital payments. Brazil's central bank reports that Pix reached nearly 170 million users and processed BRL 11 trillion in transactions in 2024 — making instant payment and fast driver settlement table stakes for any Brazil deployment.

The practical requirement: ride-hailing software must handle both realities simultaneously. That means supporting cash trip workflows (driver-side tracking, reconciliation reporting, partial digital tipping) alongside local payment gateway integrations — Mercado Pago, Pix, OXXO Pay in Mexico — not just international processors that don't reflect how most LATAM riders actually pay.

Regulatory Fragmentation Across Countries and Cities

Brazil's Lei 13.640/2018 makes the structure explicit: municipalities and the Federal District have exclusive authority to regulate and inspect ride-hailing services. National launch switches don't exist — every city is its own compliance configuration.

Colombia is the sharpest cautionary example. Uber exited Colombia entirely on January 31, 2020 after a court ruling against its operating model. It returned within weeks under a different structure, but the interruption was real. Mexico City banned cash payments and added driver registration requirements in 2019, creating city-specific operational constraints that couldn't be toggled from a national settings panel.

Software that can't configure fare rules, vehicle requirements, and operational zones at the city level isn't LATAM-ready. Retrofitting city-level compliance into a platform built around national settings is an expensive, time-consuming rebuild — and it typically happens after launch, under pressure.

Safety as a Core Product Requirement

IDB research shows women account for over 50% of public transport users in Latin America and the Caribbean, yet transport systems are consistently not designed around their safety needs. For ride-hailing platforms, this translates directly to product requirements.

SOS buttons, live trip sharing, driver identity verification, anonymized calling, and women-only ride modes are not optional features. They're baseline expectations that influence whether a potential rider downloads the app at all.

Must-Have Features in Ride-Hailing Software for Latin America

Passenger App Essentials

- Real-time driver tracking with accurate ETAs

- In-app SOS with local emergency contact integration

- Spanish and Portuguese language support at minimum

- Both cash and digital payment flows within the same booking interface

- Multi-currency display for operators spanning multiple countries

Driver App Essentials

- Turn-by-turn navigation that functions offline or in low-connectivity zones (critical for secondary cities where ANATEL data shows Brazilian rural coverage at 74% vs. 85% urban)

- Flexible availability management and shift controls

- Instant or same-day payout options, which remain the single most effective driver retention lever in cost-sensitive LATAM markets

- Simplified document verification onboarding that handles local ID formats

Admin and Operations Capabilities

- City-level geofencing to define licensed service zones and enforce operational boundaries

- Surge pricing controls configurable per zone and time window

- Fleet utilization and driver performance reporting

- Manual ride assignment for corporate or pre-booked trips

- Commission and incentive program configuration without requiring developer involvement

Route Optimization and Mapping Infrastructure

The routing and mapping layer is where most operators underinvest, and it's where LATAM deployments most visibly fail. In cities like São Paulo and Mexico City, routing accuracy directly affects driver utilization, ETA reliability, and fuel costs. A driver routed through a dead-end in a colonia wastes five minutes per trip. At scale, that's a material operational problem.

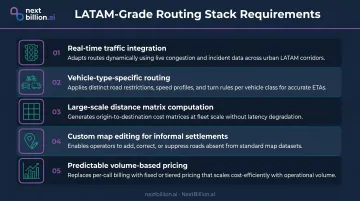

What a LATAM-grade routing stack needs:

- Real-time traffic integration for high-density urban corridors

- Vehicle-type-specific routing (motorcycles access roads sedans can't; vans can't fit where motorcycles go)

- Large-scale distance matrix computation for driver-rider matching — standard providers cap at 25×25 matrices, which forces batching that adds latency to every match

- Custom map editing capabilities for informal settlement coverage

- Predictable pricing that doesn't compound with ride volume

Each of those requirements has a direct infrastructure cost when it's missing. NextBillion.ai's routing API handles distance matrices up to 5,000×5,000 elements, processing 25 million origin-destination pairs per call versus the 625 pairs a standard 25×25 matrix supports — a gap that compounds with every matching cycle at scale. The Driver Assignment API delivers sub-second latency for nearest-driver matching, and vehicle-specific routing profiles apply appropriate road restrictions across motorcycles, sedans, and larger vehicles.

NextBillion.ai's customers include Gojek, which operates in Southeast Asian urban environments with informal settlement mapping challenges closely analogous to LATAM. The documented deployment involved merging proprietary map data with OpenStreetMap to correctly represent building entry/exit points and informal area navigation. That same approach applies directly to favelas and colonias, where address coverage gaps in standard map data translate to failed pickups and driver confusion.

Choosing or Building Your LATAM Ride-Hailing Tech Stack

Custom Development vs. White-Label Software

| Approach | Timeline | Cost Profile | Best For |

|---|---|---|---|

| Custom build | 12–18 months | High upfront | Well-funded operators targeting scale with deep localization needs |

| White-label | 2–4 months | Lower upfront, less flexibility | Startups or operators testing a new market quickly |

| API-layer assembly | Variable | Modular, scales with usage | Mid-market operators with technical capacity who need flexibility without a full rebuild |

The API-layer path is the practical choice for operators who want more control than a white-label box allows but can't absorb 18 months and significant capital to build from scratch. The tradeoff is that you own the integration risk — which means vendor selection matters: look for clear documentation, responsive technical support, and SLAs that hold under production load.

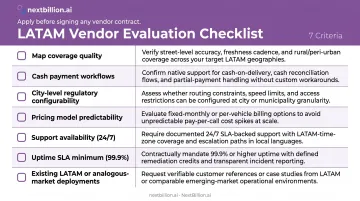

Key Evaluation Criteria for LATAM Vendors

When evaluating any ride-hailing software vendor for Latin America, apply this checklist:

- Map coverage quality — Does the vendor support custom road data ingestion for informal settlements, or does it rely purely on base map providers?

- Cash payment workflows — Native support for driver-side cash tracking and local gateway integrations (PIX, Mercado Pago, OXXO), not bolt-ons

- City-level regulatory configurability — Can fare rules, vehicle requirements, and operational zones be configured per city without a full redeploy?

- Pricing model — Per-API-call billing compounds aggressively as ride volume grows; per-vehicle or per-trip pricing is more predictable at scale

- Support availability — 24/7 access to solution engineers matters when a routing issue in São Paulo is active at 2am

- Uptime SLA — A 99.9% monthly availability commitment is the minimum acceptable for consumer-facing ride-hailing

- Existing LATAM or analogous-market deployments — A vendor who has solved informal road mapping in Southeast Asia transfers that experience directly directly to LATAM deployments

Localization Beyond Language

Translating the app into Spanish and Portuguese is the easy part. Genuine LATAM localization includes:

- Fare structures calibrated to local income levels, not US or European baselines

- Trust signals that match local expectations — driver photo prominence, community ratings, visible identity verification

- Service types that reflect local mobility modes: mototaxi, shared van (colectivo), corporate SUV, women-only

- Configurable service type creation without requiring a full platform redeploy each time a new mode is added

When adding a new service type requires a developer deployment rather than an ops-side configuration, every product adjustment carries a delay cost. In a market where mobility modes shift as fast as LATAM's, that friction accumulates quickly.

Frequently Asked Questions

What is the most popular ride-hailing app in Latin America?

Uber holds the broadest regional presence, operating across 15+ LATAM countries and maintaining the largest overall user base. DiDi leads in pricing aggression in Mexico and Brazil, while Cabify dominates premium and corporate segments across Chile, Peru, and several other markets.

What ride-hailing apps are popular in São Paulo, Brazil?

São Paulo's primary options are Uber, DiDi (which operates through its 2018 acquisition of 99), and Cabify. DiDi competes heavily on price, while Cabify focuses on corporate travel and premium positioning in Brazil's largest city.

Which rideshare apps operate in Spanish-speaking Latin American countries?

The main players across Spanish-speaking LATAM markets:

- Uber — active in 15+ countries, the widest geographic footprint

- Cabify — strong in Chile, Peru, Colombia, and Mexico; premium and corporate focus

- DiDi — active in Mexico and Colombia, competing on price

- InDriver — expanding in secondary cities with a price-negotiation model

What are the main challenges of building a ride-hailing app for Latin America?

Four problems dominate:

- Road mapping accuracy in informal settlements

- Cash payment integration with local gateways

- Regulatory variation at the city level, not just by country

- Reliable offline functionality where mobile connectivity is inconsistent

Does ride-hailing software need to support cash payments in Latin America?

Yes. Cash is still the primary payment method for a large share of riders in Brazil and Mexico, and platforms limited to digital payments exclude a significant portion of the addressable market. Supporting full cash trip workflows — not just a bolted-on cash option — is a baseline requirement.

What mapping technology works best for ride-hailing in Latin America?

Generic map providers have poor coverage of informal urban areas. LATAM operators need routing engines that support custom road data ingestion, vehicle-type-specific routing, and large-scale distance matrix computation — capabilities that providers with Southeast Asian informal-settlement experience tend to handle best.